Challenge and Opportunity

“What’s the market like?” – An often-asked question that can never be answered simply in New York City. We can generalize overall conditions, but just as the look and feel of each neighborhood in each borough in the fabric of this city differs, so too does the make-up of sellers and buyers and properties they are selling and buying across the neighborhoods of the city.

Entering our second month of 2023, we are still facing a low inventory environment in the city. Properties are hanging out longer on the market in general as buyers take longer to consider options. Yet Brooklyn boasts the greatest number of neighborhoods on the rundown of the city’s most advantageous to sellers, experiencing the most contentious bidding situations and tightest discounts from asking prices. Across the river, Manhattan has essentially remained flat on inventory year over year. For perspective, the borough had nearly 25% more active listings on the market in February 2021, and nearly 35% more properties in contract.

With the hike in interest rates, many would-be sellers have focused on re-adapting to their current homes, rather than trading out of their low interest mortgages into significantly higher. This has hampered resale inventory. As we look ahead, the increase of filings for new development units with the city in 2022 will ease some of the dearth of resale inventory as their availability becomes a reality, but that’s looking 18-24 months out.

What we are currently seeing as a trend now in the last 2-3 weeks is a notable increase in buyer inquiries for appointments to view on market listings, general inquiries to field questions about those listings and weekend open house attendance. Likewise, there was a 25% increase two weeks ago in weekly mortgage applications, followed by a 7% increase last week. Mortgage interest rates in general have slid down to a 4-month low. Buyers seem to be adapting to this new normal.

We’ve clocked a month of the new year, emerged from the holiday months, and if the street-level increase in buyer activity is followed with an increase in buyer-decisiveness, it will translate into an increase in sales activity in the next quarter. We will have to wait for the results.

In the meantime, we’ve seen some buyers in the last month trailing the trend of increased activity and decide to hold their search, remain fairly passive or make below market offers that continue to prove futile. As the next quarter unfolds, we suspect for those buyers who have adapted those habits in the last few months but are focused neighborhoods that have been historically competitive, their approach will translate into frustration as they pass up good opportunities and lose out on purchases to more assertive buyers – likely at pricing that is only moderately higher, but regrettably close.

-----------

The Numbers

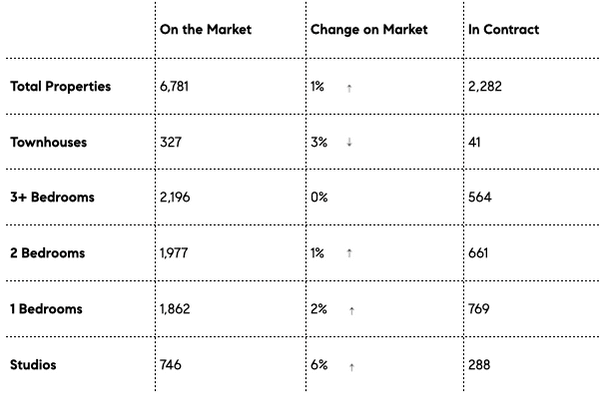

Manhattan Market Activity

Highlighting our market's past 30 days.

---------

The Properties

Our month's featured listings on the market.

Brooklyn Heights / Brooklyn

Coop

3 Beds / 2 Baths

$2,600,000

Upper East Side / Manhattan

Coop

1 Bed / 1 Bath

$745,000

West Village / Manhattan

8 Beds / 9 Baths

Townhouse

$8,750,000

Downtown Brooklyn / Brooklyn

1 Bed / 1 Bath

Condo

$645,000

------------------

The Pick

From the cool and eccentric to reserved and irreverent - Our month's pick of what's happening in New York City.

If you haven't already, you should:

Titanic: The Exhibition

Immerse yourself in over 200 artifacts,

personal stories and life-sized

recreations of the ship's interior.